HSA Tax Advantage for Self-Employed in 2026: Unlock 15% Savings

As a self-employed individual, navigating the complex world of healthcare and taxes can often feel like a juggling act. Every dollar saved and every tax advantage leveraged contributes directly to your bottom line and financial security. In this intricate landscape, the Health Savings Account (HSA) stands out as an exceptionally powerful tool, especially for the self-employed, offering a significant HSA self-employed 2026 tax advantage that could be as high as 15% or even more, depending on your tax bracket and state of residence. This comprehensive guide will delve deep into the nuances of HSAs for the self-employed in 2026, exploring how you can harness this incredible financial instrument to not only cover your healthcare costs but also build a robust retirement nest egg.

The year 2026 brings with it updated figures, rules, and perhaps subtle shifts in the economic environment that make understanding HSAs more critical than ever. For those operating outside traditional employer-sponsored health plans, the HSA is not just a savings vehicle; it’s a strategic financial pillar. It offers a unique triple tax advantage: tax-deductible contributions, tax-free growth of investments within the account, and tax-free withdrawals for qualified medical expenses. This trifecta makes the HSA arguably one of the most tax-efficient accounts available today, particularly for the self-employed who bear the full brunt of healthcare costs and tax obligations.

Let’s embark on a detailed exploration of how the HSA self-employed 2026 landscape can be optimized for your benefit, ensuring you’re well-equipped to make informed decisions for your health and financial future.

Understanding the Basics of an HSA for the Self-Employed in 2026

Before we dive into the specific advantages for the self-employed, let’s establish a foundational understanding of what an HSA is and its core requirements. A Health Savings Account is a tax-advantaged savings account that can be used for healthcare expenses. To be eligible for an HSA, you must be covered by a High Deductible Health Plan (HDHP). For 2026, the IRS will release updated figures for what constitutes an HDHP, but generally, these plans have higher deductibles than traditional insurance plans and lower monthly premiums.

Eligibility Criteria for Self-Employed Individuals

The eligibility rules for an HSA self-employed 2026 are largely the same as for employed individuals, but with specific considerations for your self-employment status:

- High Deductible Health Plan (HDHP) Enrollment: This is the cornerstone of HSA eligibility. You must be covered by an HDHP as of the first day of the month for which you want to make contributions. For self-employed individuals, this typically means purchasing an HDHP through the Health Insurance Marketplace (healthcare.gov), a private insurer, or a health sharing ministry that qualifies as an HDHP for HSA purposes.

- No Other Health Coverage: Generally, you cannot be covered by any other health plan that is not an HDHP. This includes Medicare, TRICARE, or other traditional health insurance plans. There are exceptions for specific types of coverage, such as dental, vision, disability, or long-term care insurance.

- Not Claimed as a Dependent: You cannot be claimed as a dependent on someone else’s tax return.

- Age: You must not be enrolled in Medicare.

It’s crucial for self-employed individuals to carefully review their health insurance options to ensure their chosen plan meets the HDHP criteria set by the IRS for 2026. A minor deviation could render you ineligible for HSA contributions, thereby missing out on significant tax benefits.

Contribution Limits for 2026

The IRS sets annual contribution limits for HSAs, which typically see a slight increase each year to account for inflation. For 2026, while the exact figures are not yet released, we can anticipate them to be higher than the 2025 limits. As a self-employed individual, you can contribute up to the maximum annual limit for self-only coverage or family coverage, depending on your HDHP. Additionally, if you are age 55 or older, you can make an extra $1,000 catch-up contribution per year. These limits are per individual, meaning if both you and your spouse are self-employed and eligible for an HSA under family HDHP coverage, you can each contribute a catch-up amount if applicable.

Understanding these limits is vital for maximizing your HSA self-employed 2026 savings. Contributing the maximum amount allowable each year is a powerful strategy for accumulating substantial funds for future healthcare needs and retirement.

The Unparalleled 15% (or More) Tax Advantage for Self-Employed

Now, let’s dissect the core benefit that makes HSAs so attractive for the self-employed: the significant tax advantage. While the 15% figure is a general estimate, it represents the potential tax savings for many self-employed individuals when considering the combined federal income tax, state income tax (where applicable), and the self-employment tax.

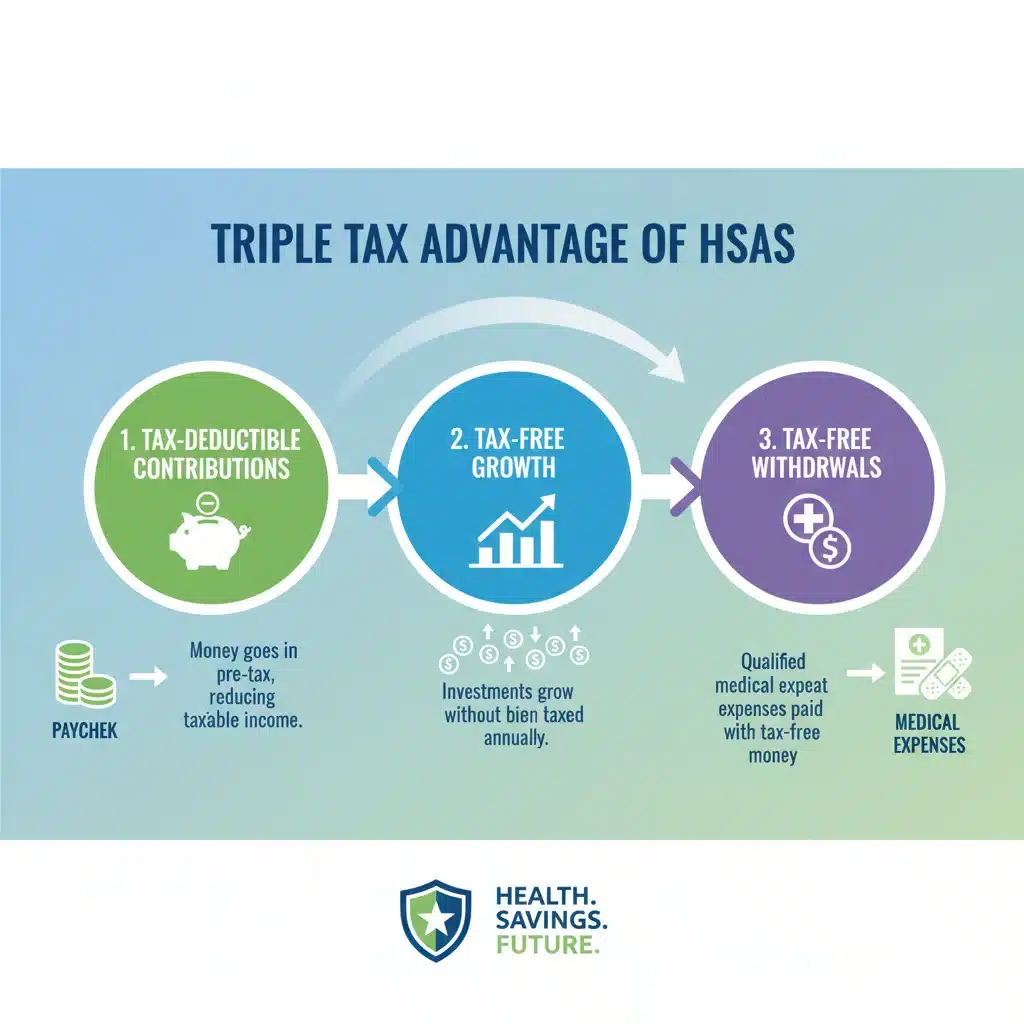

Triple Tax Advantage Explained

The HSA’s triple tax advantage is its defining feature:

- Tax-Deductible Contributions: As a self-employed individual, your contributions to an HSA are tax-deductible. This deduction is an ‘above-the-line’ deduction, meaning it reduces your Adjusted Gross Income (AGI). A lower AGI can have a ripple effect, potentially reducing your eligibility for certain tax credits or increasing your eligibility for others, and lowering your overall tax liability. This deduction directly translates to a reduction in your taxable income, saving you money on federal income taxes and, in many states, state income taxes.

- Tax-Free Growth: The funds in your HSA can be invested, and any earnings, such as interest, dividends, or capital gains, grow tax-free. This is a significant advantage, as it allows your money to compound more rapidly compared to taxable investment accounts. Over decades, this tax-free growth can lead to a substantial sum.

- Tax-Free Withdrawals for Qualified Medical Expenses: When you use your HSA funds for qualified medical expenses, the withdrawals are entirely tax-free. This includes a wide range of expenses, from doctor’s visits and prescriptions to dental care, vision care, and even long-term care insurance premiums. This means you’re paying for healthcare with money that has never been taxed, maximizing the purchasing power of your funds.

The Self-Employment Tax Factor

For the self-employed, there’s an additional, often overlooked, layer to the HSA tax advantage: the self-employment tax. Self-employment tax includes Social Security and Medicare taxes, totaling 15.3% on net earnings up to a certain threshold, and 2.9% for Medicare on earnings above that. While HSA contributions do not directly reduce your self-employment tax liability, the deduction for health insurance premiums (which can include HDHP premiums) and the overall reduction in AGI can indirectly impact your financial picture. More importantly, the ability to pay for healthcare with pre-tax dollars effectively reduces the amount of post-tax income you need to allocate to these expenses, indirectly preserving more of your earnings that would otherwise be subject to self-employment tax.

Consider this: if you’re in the 12% federal income tax bracket and your state has a 3% income tax, your combined marginal tax rate is 15%. If you contribute $3,850 (the 2023 individual limit, used here for illustration) to your HSA self-employed 2026, you could save approximately $577.50 in taxes directly. This doesn’t even account for the tax-free growth and withdrawals, which amplify the savings over time. For those in higher tax brackets, the percentage saved is even greater.

Strategic Uses of Your HSA as a Self-Employed Individual

Beyond simply paying for current medical expenses, an HSA can be a cornerstone of your long-term financial planning as a self-employed professional.

The HSA as a Retirement Savings Vehicle

Many financial advisors refer to the HSA as the ‘super Roth IRA’ or the ‘ultimate retirement account’ due to its triple tax advantage. Unlike a 401(k) or IRA, where you typically get a tax deduction on contributions or tax-free withdrawals in retirement, the HSA offers both (when used for qualified medical expenses). If you’re fortunate enough to have few medical expenses in your younger years, you can pay for current medical costs out-of-pocket and allow your HSA funds to grow untouched. Keep meticulous records of all your qualified medical expenses, as you can reimburse yourself tax-free from your HSA at any point in the future, even decades later. This strategy essentially turns your HSA into a tax-free investment account that you can tap into for tax-free reimbursements later in life, or for general retirement income after age 65 (though withdrawals for non-medical expenses after 65 are taxed as ordinary income, similar to a traditional IRA).

Covering High Deductibles and Unexpected Medical Costs

The primary purpose of an HSA is to help you cover the high deductible of your HDHP. As a self-employed individual, you are responsible for your entire deductible before your insurance begins to pay. Having a robust HSA balance means you’re prepared for unexpected medical emergencies or planned procedures, mitigating the financial stress that can come with high out-of-pocket costs. This financial buffer is invaluable for maintaining peace of mind and business continuity.

Funding Future Healthcare in Retirement

Healthcare costs in retirement can be substantial. Fidelity estimates that a couple retiring at age 65 in 2023 would need approximately $315,000 to cover medical expenses throughout retirement. An HSA self-employed 2026 can be a powerful tool to save specifically for these future costs. Even after you enroll in Medicare, you can use your HSA funds to pay for Medicare premiums (Parts B, C, and D), deductibles, co-pays, and coinsurance. You can also use it for qualified long-term care insurance premiums. This makes the HSA an indispensable component of a comprehensive retirement plan.

Choosing the Right HDHP for Your HSA

Selecting the appropriate High Deductible Health Plan is paramount to unlocking the benefits of an HSA self-employed 2026. This decision involves more than just finding the lowest premium; it requires a careful evaluation of your anticipated healthcare needs, risk tolerance, and financial situation.

Key Considerations When Selecting an HDHP:

- Deductible Amount: While all HDHPs have high deductibles, the specific amount can vary. Understand what your out-of-pocket maximum will be, as this is the most you would pay in a calendar year for covered services.

- Network: Ensure the plan’s provider network includes your preferred doctors, specialists, and hospitals. As a self-employed individual, continuity of care can be crucial.

- Preventive Care: HDHPs are required to cover certain preventive services at 100% before the deductible is met. Familiarize yourself with what’s included.

- Drug Coverage: Review the plan’s formulary to understand how your prescription medications would be covered, especially if you have ongoing prescriptions.

- Premium vs. Deductible: Balance the monthly premium cost with the deductible and out-of-pocket maximum. A lower premium might mean a higher deductible, requiring you to have more funds readily available in your HSA.

The Health Insurance Marketplace (healthcare.gov) is an excellent resource for self-employed individuals to compare HDHPs and determine eligibility for subsidies that could significantly reduce premium costs. Even with subsidies, choosing an HDHP allows you to pair it with an HSA, maximizing your tax advantages.

Managing Your HSA: Contributions, Investments, and Withdrawals

Once you’ve established your HSA self-employed 2026, effective management is key to realizing its full potential.

Making Contributions

As a self-employed individual, you are responsible for making your own contributions. You can typically do this through electronic transfers from your bank account to your HSA custodian. It’s often beneficial to set up recurring contributions, similar to how you might fund a retirement account, to ensure you consistently meet your savings goals and maximize your tax deduction.

Remember that you can contribute to your HSA up until the tax filing deadline for the previous year (typically April 15th) and still have those contributions count for the prior tax year. This flexibility can be particularly useful for year-end tax planning.

Investing Your HSA Funds

Many HSA providers offer investment options once your account reaches a certain cash threshold. This is where the tax-free growth truly comes into play. For long-term growth, consider investing your HSA funds in a diversified portfolio of low-cost index funds or ETFs, similar to how you might invest in a 401(k) or IRA. The longer your investment horizon, the greater the potential for compounding returns.

When choosing an HSA provider, consider:

- Investment Options: What range of investment choices do they offer?

- Fees: Are there monthly maintenance fees, investment fees, or trading commissions?

- Ease of Use: How user-friendly is their online platform for managing contributions, investments, and withdrawals?

Qualified Medical Expense Withdrawals

Keeping meticulous records of all your qualified medical expenses is crucial. This includes receipts for doctor’s visits, prescriptions, dental work, vision care, and even mileage for medical appointments. You can pay for these expenses directly from your HSA with a debit card or check, or you can pay out-of-pocket and reimburse yourself later. The latter strategy, known as ‘investing and deferring,’ allows your HSA funds to grow tax-free for longer, providing a larger tax-free sum when you eventually reimburse yourself.

The IRS defines qualified medical expenses broadly, but it’s always wise to consult IRS Publication 502, ‘Medical and Dental Expenses,’ for a comprehensive list and any updates for 2026. Incorrect withdrawals for non-qualified expenses can lead to taxes and penalties.

Common Pitfalls and How to Avoid Them

While the HSA self-employed 2026 offers immense benefits, there are a few common mistakes that self-employed individuals should be aware of to avoid potential issues.

Missing HDHP Eligibility

The most common pitfall is contributing to an HSA without being covered by a qualifying HDHP. This can happen if your plan doesn’t meet the deductible or out-of-pocket maximum requirements, or if you have other disqualifying coverage. Always confirm your HDHP status with your insurance provider and review IRS guidelines annually.

Over-Contributing

Exceeding the annual contribution limits can lead to a 6% excise tax on the excess contributions. Keep a close eye on the IRS limits for 2026 and track your contributions carefully. If you accidentally over-contribute, you can withdraw the excess amount and any earnings on it before the tax filing deadline to avoid penalties.

Lack of Investment

Many HSA holders treat their accounts like a regular checking account, letting funds sit in cash. While this provides liquidity for immediate expenses, it misses out on the powerful tax-free growth potential. If you’re able, invest your HSA funds for long-term appreciation.

Poor Record Keeping

If you plan to use the ‘investing and deferring’ strategy, maintaining detailed records of all qualified medical expenses is absolutely critical. Without proper documentation, you may not be able to justify tax-free reimbursements in the future, potentially leading to taxable income and penalties.

HSA vs. Other Self-Employed Retirement Options

For self-employed individuals, there are several excellent retirement savings options, including SEP IRAs, Solo 401(k)s, and traditional/Roth IRAs. The HSA isn’t necessarily a replacement for these but rather a powerful complement.

- HSA vs. SEP IRA/Solo 401(k): SEP IRAs and Solo 401(k)s allow for much higher contribution limits, making them ideal for high-income self-employed individuals to save significantly for retirement. However, they don’t offer the triple tax advantage for healthcare expenses that an HSA does. The ideal strategy is often to maximize your HSA contributions first, then contribute to a SEP IRA or Solo 401(k) to further boost your retirement savings.

- HSA vs. Traditional/Roth IRA: Traditional and Roth IRAs are excellent personal retirement accounts. A Traditional IRA offers tax-deductible contributions (for those who qualify), and a Roth IRA offers tax-free withdrawals in retirement. The HSA combines elements of both, providing a deduction on contributions and tax-free withdrawals for medical expenses, making it uniquely powerful.

By integrating an HSA self-employed 2026 into your overall financial plan, you create a diversified approach to saving for both healthcare and retirement, leveraging the unique tax benefits of each account type.

The Future of HSAs for the Self-Employed Beyond 2026

While we’re focusing on 2026, it’s worth considering the long-term outlook for HSAs. Historically, HSAs have enjoyed strong bipartisan support due to their emphasis on consumer-driven healthcare and tax-advantaged savings. While specific rules and contribution limits may evolve, the core benefits of the HSA are expected to remain a staple of the U.S. tax code.

Staying informed about legislative changes and IRS updates is crucial for self-employed individuals. Subscribing to financial news outlets, consulting with a tax professional or financial advisor, and regularly checking the IRS website will ensure you’re always operating with the most current information regarding your HSA self-employed 2026 and beyond.

Actionable Steps for Self-Employed in 2026

- Review Your Health Insurance: Confirm that your current or prospective health insurance plan meets the IRS definition of an HDHP for 2026. If not, explore options on the Health Insurance Marketplace or through private insurers.

- Open an HSA: If you’re eligible, open an HSA with a reputable provider that offers competitive fees and investment options.

- Set Up Contributions: Establish a plan to contribute consistently, aiming to max out your contributions each year if possible. Consider setting up automatic transfers.

- Invest Your Funds: Once you have a comfortable cash cushion for immediate medical expenses, invest the remainder of your HSA funds for long-term growth.

- Keep Meticulous Records: Document all qualified medical expenses, even those you pay out-of-pocket, for potential future tax-free reimbursements.

- Consult Professionals: Work with a financial advisor and/or tax professional who understands the unique financial landscape of the self-employed to integrate your HSA into your broader financial and retirement strategy.

Conclusion

For the self-employed, the Health Savings Account is far more than just a savings account for medical bills; it’s a powerful and flexible financial instrument offering a significant HSA self-employed 2026 tax advantage that can reach 15% or more. By understanding its eligibility requirements, contribution limits, and strategic uses, you can leverage your HSA to not only manage your current healthcare costs but also to build a substantial, tax-advantaged fund for future medical needs and a secure retirement.

In an environment where every tax deduction and investment growth opportunity counts, the HSA stands out as an indispensable tool for the financially savvy self-employed individual. Take the time now to evaluate your options, make informed decisions, and secure a healthier, wealthier future with your Health Savings Account.